KPJ Healthcare's True Value 31% Higher

We will show you how to estimate KPJ Healthcare Berhad's intrinsic value. We'll do this by predicting its money coming in and then subtracting any costs to get the net cash flow. We'll use the DCF model. It's not too hard, even if it feels like it.

Keep in mind that there are various ways to determine a company's worth, and DCF is merely one approach. If you want to learn more about the intrinsic value, check out the Simply Wall St analysis model.

Have a look at our new study for KPJ Healthcare Berhad. The analysis provides insights into this healthcare provider. It covers various financial metrics and ratios. These include revenue growth, net income margins, and return on equity. Overall, the study presents a positive outlook for the company. It indicates strong financial performance and growth prospects. Investors and stakeholders may find this analysis helpful. It can assist in decision-making and provide valuable information for future investments.

"Is KPJ Healthcare Berhad's Valuation Fair?"

We use 2-stage growth model. It considers 2 stages of company's growth. Stage one could have higher growth, stage two has a stable growth. We need to estimate cash flows in the first stage for next ten years. We use analyst estimates or previous free cash flow for estimation. Companies with shrinking free cash flow will slow rate of shrinkage. Companies with growing free cash flow will have slower growth. Growth rate slows more in initial years.

A DCF is based on the notion that a dollar later is worth less than a dollar now. We lower the value of future cash flows to approximate their worth in present-day dollars.

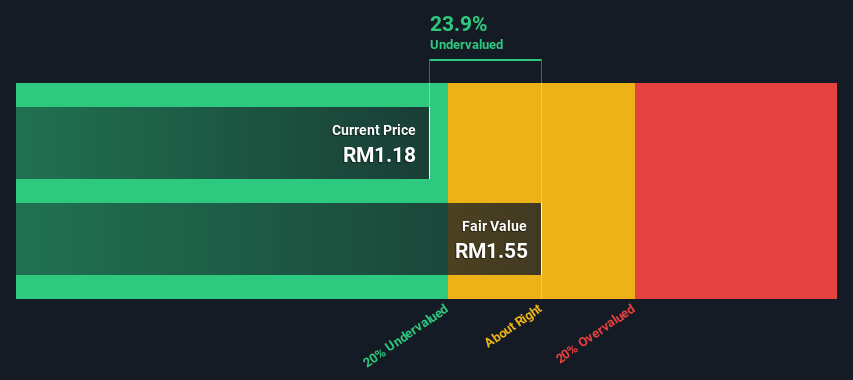

The PVCF for 10-year cash flow is RM3.4b. This value is based on the estimated FCF growth rate calculated by Simply Wall St which is denoted as "Est".

In stage 2, we talk about Terminal Value. It's the biz's cash flow after stage 1. We use a formula called Gordon Growth to work out the Terminal Value. It's based on a future growth rate of 3.6%, which is the 5-year average of the 10-year gov bond yield. We bring today's value to the Terminal cash flows by taking a discount at a rate of 12%.

The Terminal Value is calculated by multiplying FCF2032 with (1 + g) and dividing it by (r - g). The value comes to RM10b using the given values of RM785m for FCF2032, 3.6% for growth rate (g) and 12% for discount rate (r).

The PVTV is a calculation that finds the current value of a future sum of money. It's found by dividing the Terminal Value by (1 + r) to the 10th power. In this case, the Terminal Value is RM10b and the interest rate (r) is 12%. After doing the calculation, the PVTV is found to be RM3.4b.

The equity value is RM6.8b. To get the value per share, divide it by the total shares. The company seems undervalued at a 24% discount. Calculations are assumptions and not precise.

We base our calculation on two assumptions: discount rate and cash flows. It's important to make your own evaluation of a company's future performance and check your assumptions. The DCF doesn't take into account cyclicality or future capital requirements. For KPJ Healthcare Berhad, we use the cost of equity as the discount rate. Our discount rate is 12% based on a levered beta of 1.002. Beta measures a stock's volatility compared to the market. We use the industry average beta with a limit of 0.8 to 2.0 for a stable business.

"Assessing KPJ Healthcare: SWOT Analysis"

Company valuation is important but not the only thing to consider when researching a company. DCF model alone isn't perfect for accurate valuations. Apply various assumptions and cases to see how it impacts the company's worth. Small changes can have a significant impact. Why is the share price below the intrinsic value for KPJ Healthcare Berhad? Consider three pertinent elements.

Simply Wall St updates the DCF calculation for every Malaysian stock daily. You can find the intrinsic value of any other stock by searching here.

Simplifying Valuation: Our Mission

Want to know if KPJ Healthcare Berhad is overpriced or underpriced? Check our complete analysis. We cover fair value estimates, risks, dividends, insider transactions, and financial health. Get the information you need.

Check out the analysis for free. Find Out More Learn more about the service. Get Started Today Begin using the service today. Save Time Save your time with the service. Easy to Use The service is simple to use. Increase Efficiency Increase your efficiency with the service. Achieve Your Goals Achieve your goals with the service. Improve Your Results Improve your results with the service. Join Now Join the service now.

Want to share your thoughts on this article? Worried about what you've read? Contact us right away. You can also send an email to editorial-team (at) simplywallst.com.

This post from Simply Wall St is general. We just talk about past data and predictions using an unbiased method. We're not giving financial advice. We're not suggesting to buy or sell any stocks, and we don't consider your goals or money situation. We want to give you long-term analysis using fundamental facts. Keep in mind that we might miss the latest company updates or opinions. Simply Wall St doesn't have any stocks mentioned.